Evolv Technologies ($EVLV)

Disrupting entrance security with cutting-edge tech

Make your portfolio reflect your best vision for our future.

— David Gardner

As a good rule of thumb, proprietary technology must be at least 10 times better than its closest substitute in some important dimension to lead to a real monopolistic advantage. Anything less than an order of magnitude better will probably be perceived as a marginal improvement and will be hard to sell, especially in an already crowded market.

— Peter Thiel (Zero to One)

Evolv price today (February 18, 2025): $3.52 USD

Market cap: $556.9M USD

Evolv Technologies appears to be a high-quality business, and I find it hard to envision a scenario in which an investment at today’s prices fails to deliver market-beating returns (although I've been wrong before — see my pitch on Payfare).

What does Evolv do?

Evolv develops contactless security screening solutions that use sensor technology to detect potential threats. Its system, the Evolv Express™, allows for real-time entrance screening in high-traffic environments such as airports, stadiums, and large event venues, enhancing both efficiency and safety.

The systems resemble metal detectors, but instead use radio frequency (RF) electromagnetic sensors to scan individuals as they pass through the system. The collected data is processed by algorithms that differentiate between potential threats and innocuous items like phones and keys.

Here are a couple of images of the product and what an operator would see when a potential threat is detected:

The company reminds me a bit of Zedcor — another security hardware company with a recurring revenue component — but with a better, proprietary product. Disclosure: I also own Zedcor and I've shared my thoughts on it, including the unit economics of Zedcor’s Towers (>40% estimated IRR) in a previous blog post.

Value Proposition

A couple of reasons why Evolv’s systems are superior to traditional metal detectors:

They allow you to pinpoint where on the body a potential threat is located; and

Most importantly, they enable up to 10 times the throughput of people compared to traditional metal detectors. In part, this is because you don’t have to empty your pockets, and also because the operator knows more precisely where to focus their search.

This increased throughput can (1) create value for venues and (2) open up new use cases for entrance security in areas where traditional metal detectors may not have been considered previously.

Value creation: I have seen the screeners in action at our local hockey arena. Previously there was a long queue before every game, but since the installation of the Evolv scanners, traffic flows much quicker. Quicker entry allows the arena more time to sell food, beverages, and merchandise to patrons.

Additional use cases: The increased throughput can also improve the cost-benefit equation in settings where traditional metal detectors would cause significant delays at peak times — for example, schools, subways, and hospitals.

Evolv’s scanners are used by highly credible and discerning customers, including Disney (since 2020), multiple sports arenas (starting in 2022), and the Olympics (2024).

The company faced an FTC inquiry regarding its prior aggressive marketing claims, which was resolved on November 26, 2024. As part of the resolution, a limited group of K-12 education customers were given a 60-day window to cancel their contracts (affecting approximately 237 units). The vast majority of the cancellation rights are scheduled to expire by March 14, 2025. As of January 23, 2025, no customers had exercised their cancellation rights.

Tweets and Thoughts on Evolv

Recently I have been posting about Evolv, and other companies I own, on Twitter: https://x.com/stephendebeir

Tweet #1

I don't think it's unrealistic that most public high-schools in the United States will have an entrance security system like Evolv’s within 10 years. Per ChatGPT, there are roughly 23,800 public high schools in the US and Evolv has penetrated less than 2,000 thus far; this is just one vertical.

Another excerpt from a news article posted last week:

Evolv is also starting to sell their newly released bag scanning product, the Evolv eXpedite™, into schools which pairs with their walk-through scanners. This new product hints at the company’s potential optionality, although it is too early to tell viability of this product.

Tweet #2

Often after a school or hospital installs an Evolv scanner there is a news story published about it. This is a business model quality I really like, which I also noted in my Trustpilot pitch → customers and users are essentially advertising Evolv’s products for free, leading to increased marketing efficiency and higher ROIC.

Note: Please reach out to me at stephen@debeir.ca, or through Substack, if you know of companies that you think are worthwhile investments and (1) exhibit this quality OR (2) have high per unit IRR.

Tweet #3

Here is a similar post from Stoic Point Capital Management highlighting end-users pushing for the use of Evolv’s scanners. Their page on X is worth following if you want to see the flow of published contract wins, although reading frequent news stories like these can sometimes create false conviction (recency bias).

Napkin Valuation

The company is transitioning from a business model that sells hardware bundled with a subscription to a hybrid between a (1) pure subscription / leasing model; and (2) an outsourced licensing model (where a select vendor sells the hardware). This shift makes Evolv’s financials particularly challenging to project, but should lead to higher gross margins.

Assumptions:

Estimated FCF margin at maturity = 25%

Estimated valuation in 10 years: 20 times FCF (average)

TTM Revenue = $89.2M

Current Market Cap = $556.9M

In order for us to achieve a 20% return based on the above assumptions, the company would have to grow revenue by approximately 23% on average over the next 10 years (calculation below).

$556.94M * (1 + 20%) ^ 10 = $3,448M market cap in Year 10

$3,448M / 20 FCF multiple / 25% FCF margin = $690M Revenue in Year 10

($690M / $89.2M) ^ (1/10) - 1 = 23% required revenue growth

This doesn’t factor in share issuances or cash-returns to shareholders (buybacks / dividends) between now and then.

If FCF margins are higher at maturity; if the market applies a higher multiple of FCF, or; if revenue growth is higher than 23% then our return could be even higher than 20%. Of course the inverse would lead to a lower return.

As I’ve said before, disruptors tend to surprise to the upside.

Now I know what you’re thinking… “but Evolv’s revenue growth has slowed and was below 23% in 3 out of the last four quarters!”

This is partly due to their business model transition from a hardware sales model to pure-subscription → hardware sales provide a large, upfront, low-margin revenue stream with a small subscription fee. Whereas the pure subscription model has a smaller upfront fee, if any, and the higher-margin revenues are spread out over the life of the contract.

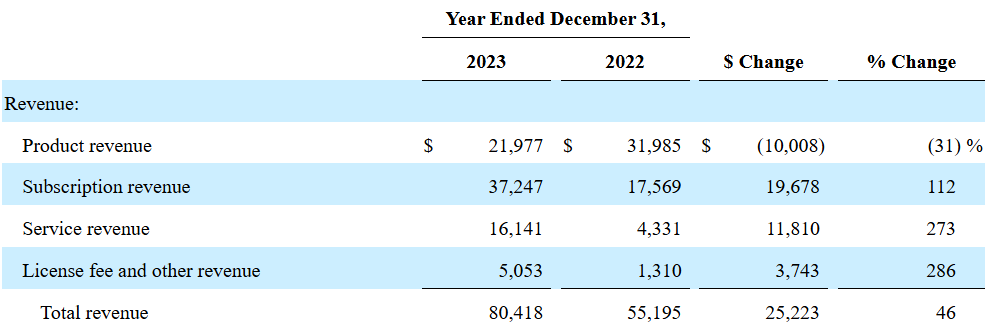

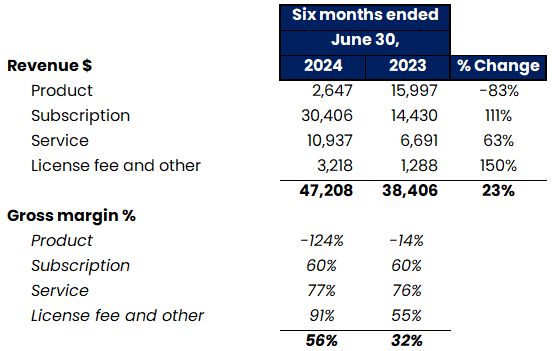

We can see this in the financial statements, take a look at the year-over-year ‘% Change’ for each segment below, the transition has put a drag on overall revenue growth:

I think we will see revenue growth re-accelerate in the coming quarters at the same time as overall margins improve.

The company added 465 subscriptions in Q3-2024 and 470 subscriptions in Q4-2024. If we annualize these amounts we get 1,870 scanners added to a base of 5,323 at the end of Q2-2024. This would suggest high-margin growth of 35% YoY (ignoring churn), and does not factor in their latest unit cost reductions (can also pass on lower costs to customers), or new products like the bag scanner.

Unit economics

Ok, customers are buying the security systems, but will Evolv make any money?

Short answer: YES

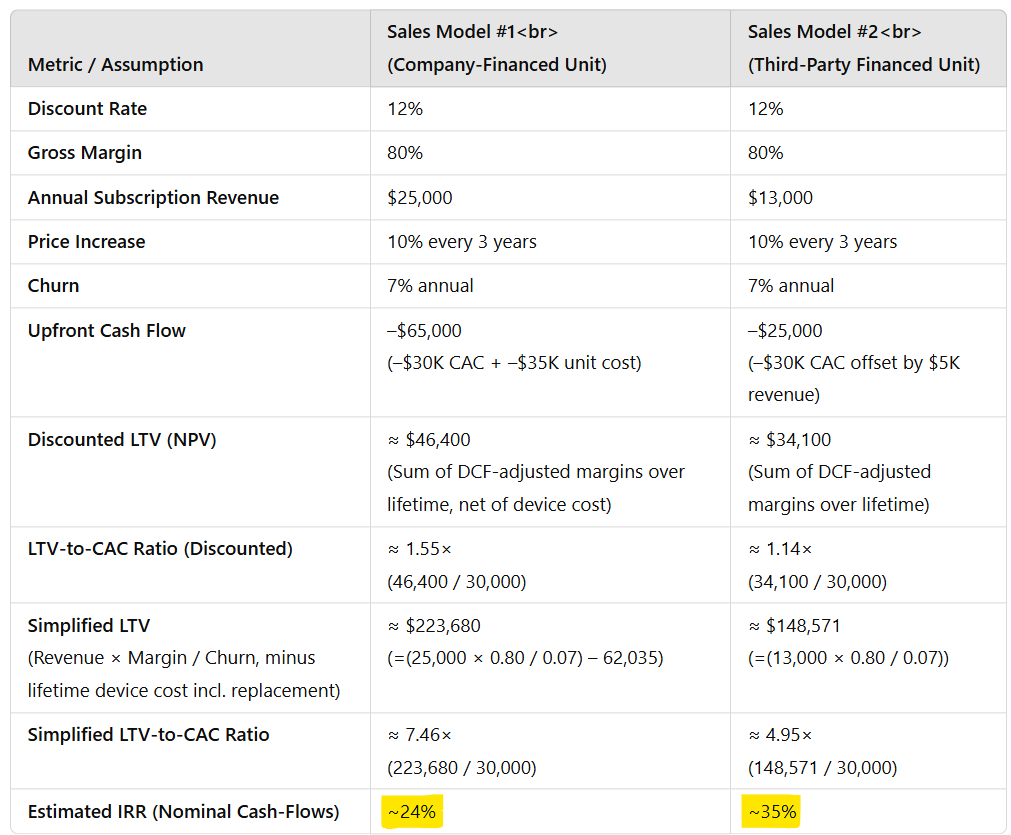

I input high-level assumptions, including some pulled from Paris Analyst’s post, into ChatGPT to estimate what Evolv’s internal rates of return (IRR) per unit might be (I also recalculated the results for reasonability).

To get a very rough estimate for CAC, I took Evolv’s total marketing spend since 2022 and divided by the total units deployed. The results are below:

Disclaimer: The above uses high level assumptions and illustrates a scenario in which the units could have high returns on investment — a sanity check. I've included my assumptions so you can assess yourself whether they are too aggressive or conservative.

Based on the above, both of Evolv’s new sales models could produce IRR in excess of 20% which would be quite good. Theoretically the long-term performance of a stock should trend towards its IRR/return on capital rates.

As we get more quarters under the new sales models we will be able to refine our calculations. Here are a few considerations I’m thinking about meanwhile:

If the systems cost $25K/year or $13K/year + upfront hardware cost (excluding labour). This doesn’t feel like a significant expense for customers to budget for in Evolv’s current target markets (schools & hospitals).

CAC could decrease as the company scales and gains efficiencies under new leadership. This would increase IRR.

We know they significantly reduced the cost of their units recently. This would (1) increase IRR and/or (2) if they pass savings on to customers, increase sales growth/reduce churn.

I used 80% as a ball-park gross margin figure (excluding depreciation). I calculate margins slightly higher than 80% in Evolv’s historical financials, but Paris Analyst quoted rates lower than 80%.

These unit-rate models are particularly sensitive to customer churn rates. Even if a customer churns, in the pure-subscription model Evolv could re-purpose the equipment and in this case we should factor in unit down-time. Churn rates are primarily influenced by customer satisfaction (value/service) and competition.

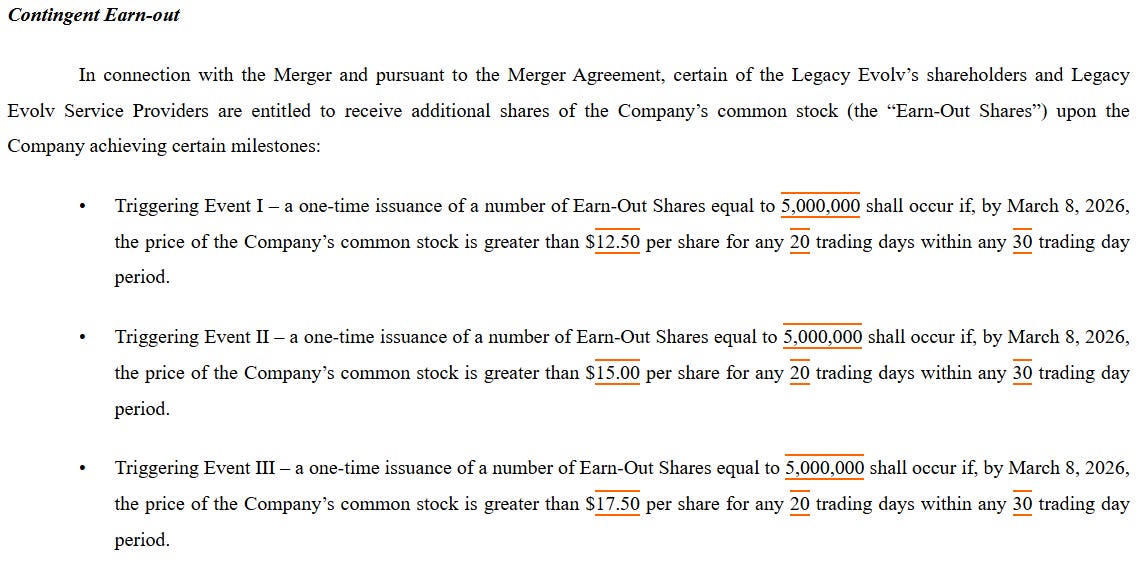

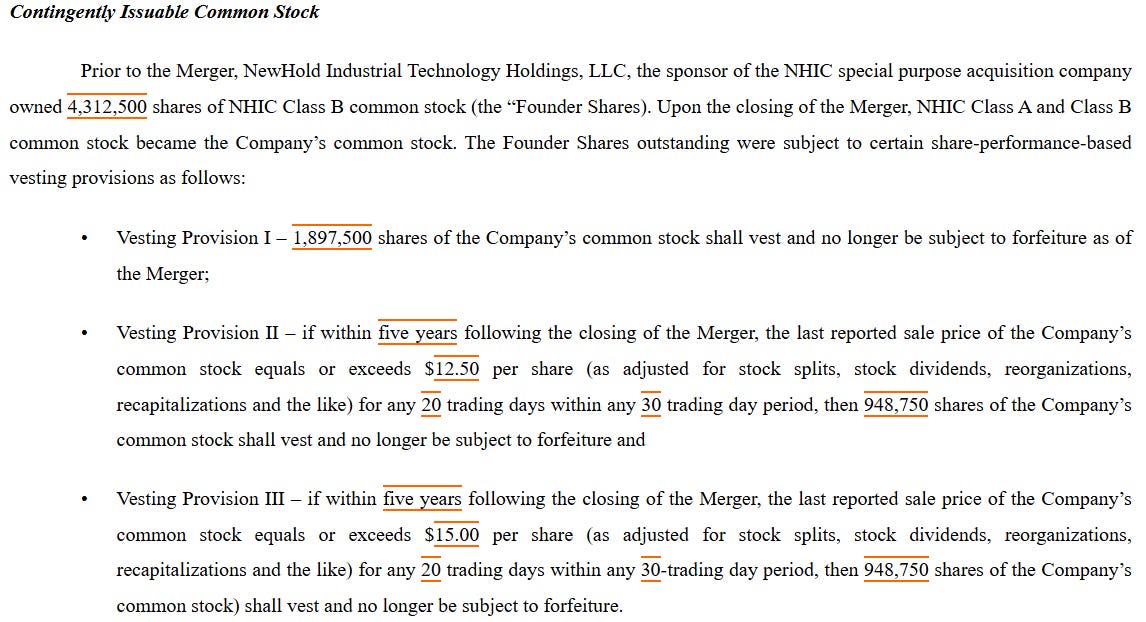

Legacy Shareholder and Founder Contingent Shares

There are a significant number of earn-out shares set to expire in March and July 2026 → we're talking between $74M and $251M depending on which thresholds are hit ($12.50 to $17.50 share price thresholds). The founders and legacy shareholders will have every incentive to succeed and have the share price increase.

Achieving, or even just approaching, these share prices would represent a significant appreciation from today's level and I don’t think it’s out of the realm of possible outcomes.

Destination Analysis

Destination analysis is a useful tool for identifying long-term compounders, and it is how I identified some of the other companies I own, including Hims and Hers, Lemonade, and Trustpilot.

I ask myself: is it plausible that this company can 10X in 10 years (26% CAGR)?

I believe that given Evolv's disruptive product and the large & growing total addressable market (security is becoming more and more of a focus in society), such an outcome is possible.

Other Considerations

(1) Liquidity:

I think I'm comfortable with the cash-flow risk now as, based on the latest business update, Evolv has (1) cash on hand of $52 million and no debt as of December 31, 2024; (2) an expectation to be free cash-flow positive by Q4; and (3) has been focusing on rationalizing operating expenses, including a 14% reduction in staff.

(2) What about management?

Evolv parted ways with their CEO and CFO after the company’s recent accounting irregularities.

The company filed a notice of late filing for its September 10-Q and their December-24 10-Q may be delayed as well. As a result, Evolv has engaged consultants (Alix Partners) to help catch up on their reporting and hire a new CFO.

Assuming the press releases are accurate, these accounting irregularities do not overly concern me. However, potential investors might choose to wait until the financials are up to date. Here were my initial thoughts from a MicroCapClub post in October (which was also posted in my chat):

I don't know much about the new CEO, John Kedzierski, which could be a risk given the limited history we have about his capital allocation and decision-making. However, we have seen some promising early signs e.g. his focus on reducing unnecessary operating expenses.

John has 16 years of experience at Motorola in various roles and I believe John's value will, at least in part, stem from his ability to attract top talent to Evolv. For example, see linked article for details on their new Chief Revenue Officer hire.

The Pareto principle is alive and strong in large companies like Motorola, where 20% of employees tend to produce 80% of the work, and when you encounter one of these 20%’ers you can usually tell who they are fairly quickly.

Even though we will have a new CEO and CFO, most importantly, Evolv still has its two co-founders, Mike Ellenbogen & Anil Chitkara, who created Evolv and grew it to what it is today.

(3) Competition:

While Evolv does have a number of competitors, their product appears to be the premium option in the industry. Given the critical nature of security products, customers may be less likely to compromise on quality. Additionally, the company's impressive growth and retention metrics suggest that competitors have yet to catch up.

Further Reading

If you’re interested in further reading on Evolv, I recommend the following article from Paris Analyst, which delves into the competitive landscape (see his detailed response in the comment section) and provides select inputs on the unit economics of the systems: https://parisanalyst.substack.com/p/evlv-our-favorite-2024-black-friday

Background on Evolv’s founding story: https://evolv.com/resources/blog/the-road-to-now/

Disclaimer: As of February 18, 2025, I am a shareholder of Evolv Technologies Holdings Inc. I am not an investment or financial advisor. My plan at the time of writing is to hold these shares long-term, but I may have sold my position by the time you’re reading this. This is not a purchase recommendation and I can only hope that I’m right on 3 out of 5 (60%) investments I make — this could be one I’m wrong on. Please do your own research and double-check my data, findings, and calculations. Please also read my disclaimer and process here: Curious Investing Disclaimer and Process

Great writeup! I will write an update early next week -- the cash on cash IRR on the machines may approach mid 40s after the new cost-down. We're in a bit of an information vacuum because the mgmt team decided not to do February conferences (I thought they would, now think they do so after fixing filings ~April) -- and I still think super interesting. Cheers, PA