Payfare Inc (TSE:PAY)

A wonderful company at a fair price?

Current price (TSE: PAY): $6.62 CAD

Current market cap (TSE: PAY): $317.41M CAD

I have been thinking about this company a lot this week and I really like what I see, with a few significant risks to call out as well.

Similar to Trustpilot, another company I wrote an investment case for, Payfare came public at the height of the recent tech boom on March 19, 2021. After an initial rally to $12.69, the share price subsequently fell by almost half to its current price of $6.62.

Disclosure: As of today approximately 7% of my portfolio is in Payfare and my full public portfolio can be viewed here: Google Sheets link

Key Points:

Payfare (TSE: PAY) is a fintech company providing Earned Wage Access (EWA). Earned Wage Access is a no-cost to the employer solution that provides workers with on-demand access to earned but unpaid wages before payday.

Valuation of 13.5 EV / AEBITDA (excl. SBC add-back) as of December 31, 2023 (unaudited) with a strong balance sheet.

The company has inflected on profitability and has shown impressive revenue growth and scalability since the company was founded in 2016.

Payfare's highly scalable business model, with minimal capital expenditures and low customer acquisition costs, is supported by its software-based operations and leverage of large customers for top of funnel marketing.

Payfare has strong growth prospects, including potential expansion to new countries, new customers, and optionality of additional features or products.

15% insider ownership, with recent insider selling observed. The company took advantage of low share prices to opportunistically buy back shares, which appears to have been a good move by management.

The company faces risks such as reliance on a few large customers, accounting issues, regulation, and potential disruption from technology advancements (e.g. autonomous vehicles reducing the need for delivery drivers).

Despite risks, Payfare's strong revenue growth, low capital intensity, low customer acquisition costs, and expanding margins make it an attractive investment opportunity. I am starting with a modest position based on the risk/reward profile.

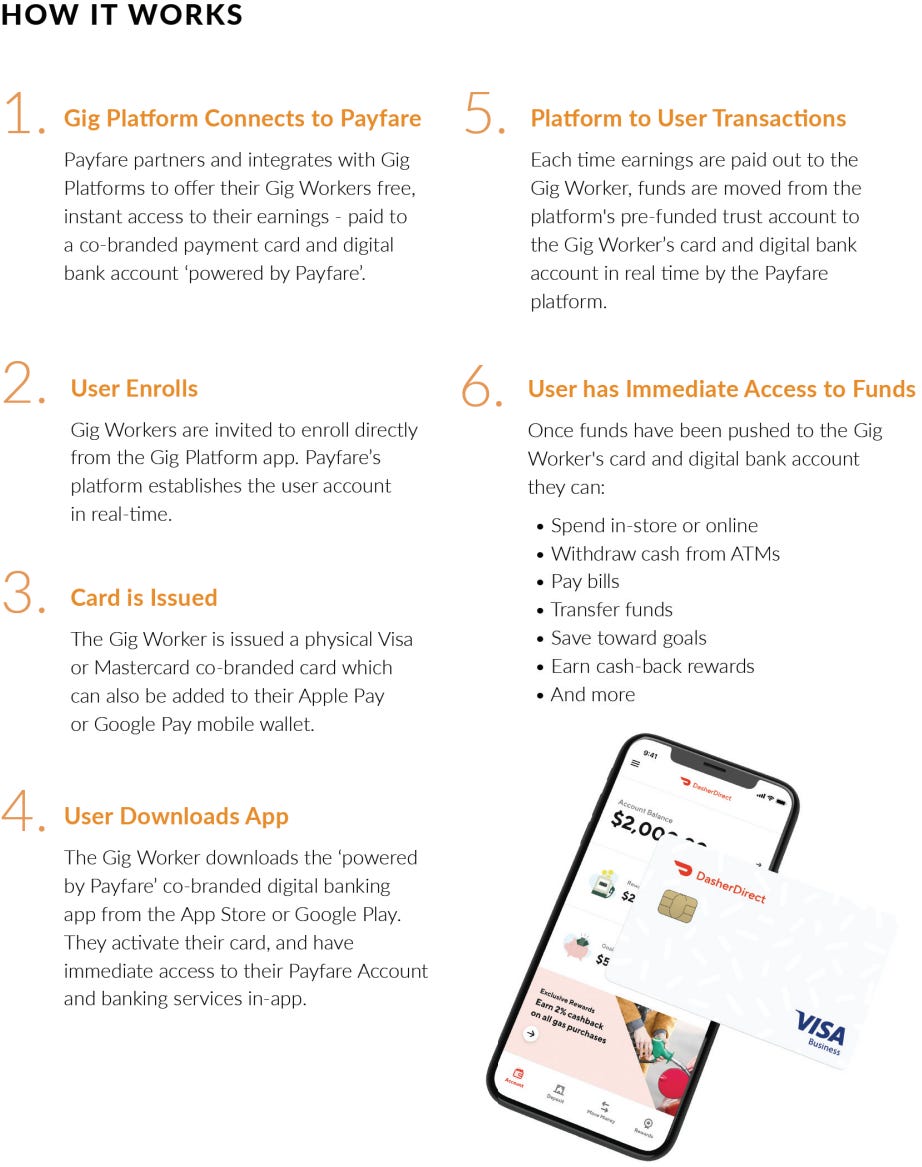

What does Payfare do?

Payfare is a financial technology (fintech) company that specializes in providing payment solutions for gig economy workers. They offer services such as instant payouts, financial wellness tools, and prepaid cards tailored to the needs of workers in the gig economy. Payfare's platform allows gig workers to access their earnings quickly and conveniently, helping them manage their finances more effectively. They plan to diversify their offering to include full-time workers as well.

Payfare currently holds contracts with much larger companies — Uber, Lyft, DoorDash, and ADP — although their contracts are limited to specific countries for now.

Payfare generates 70% - 80% of their revenue from network interchange fees from payment networks and 20% - 30% from user banking fees such as ATM withdrawals, money transfers, and foreign exchange.

I will briefly discuss the quantitative aspects of the investment case before delving more deeply into the qualitative aspects, as I think that's where we stock-pickers gain more of an edge (see my post on conviction and quality for more on this).

Valuation

Last week Payfare released their unaudited Q4 earnings in a press release. The figures are unaudited due to an outstanding vendor report (discussed in the risk section), but they do not expect the published results to change.

Payfare Announces Unaudited Fourth Quarter and Full Year 2023 Financial Results

In the press release, Payfare guides (estimates) 2024 revenue of $235M to $245M (~29% YoY) and $30M to $35M in Adjusted EBITDA (51% YoY). Side note: Earnings growing faster than revenue is a positive sign and indicates that they are in the operating leverage stage, which I will discuss later.

Current market cap: $317.41 million

Cash and equivalents: ($78.2) million (no debt)

Enterprise value (EV): $239.21 million

If we assume their intangible spending is on growth initiatives, such as onboarding integrations and adding new features such as overdraft, then EBITDA is an acceptable earnings metric to use because the company has little to no maintenance capital expenditures.

$239.21M EV / 2023 AEBITDA (excl. SBC add-back) of $17.7M = 13.5 EV / AEBITDA

$239.21M EV / 2024 AEBITDA of ~$32.5M = 7.4 EV / AEBITDA

In my opinion, the back-of-the-envelope calculation indicates to me that the current price is fair for a company with Payfare's business quality.

If you’re wondering how reliable Payfare’s forward estimates are, based on the company’s slide below, Payfare achieved its guidance in 2023 which is a good sign. They also added two significant customers post year-end (Uber Canada and ADP Canada).

Business model

Payfare is highly scalable — as a software company, they have little to no capital expenditures. So they must be bottlenecked by customer acquisition costs like a typical software company right? Wrong, their customer acquisition costs were ~2% of revenue in 2023 and ~5% in 2022, this is due to Payfare’s model of signing on large customers (Uber, Lyft, DoorDash, ADP) and using their customers' funnel to acquire users. These large customers handle the bulk of Payfare’s marketing.

The cherry on top is that all of their processing is handled by a vendor, so staff costs do not increase linearly with Gross Dollar Volume (GDV).

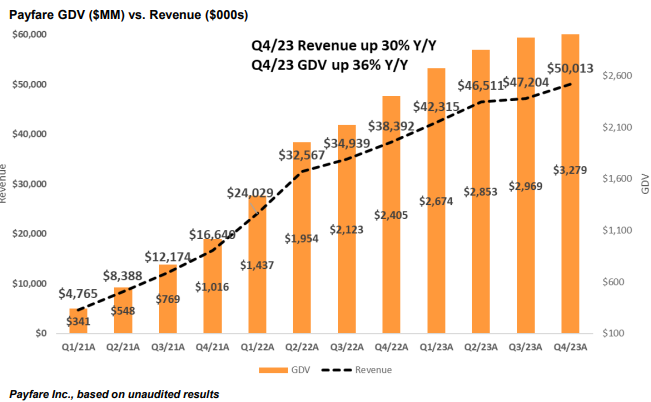

This scalability is evidenced in their historical metrics below and I don’t know many business models that can achieve such rapid revenue growth with such modest increases in operating expenses.

Payfare inflected on profitability in Q4 2022 and is currently undergoing operating leverage where earnings will rise faster than revenue, as incremental revenue is spread over fixed operating costs.

Another point to note is their gross margin expansion. This is partly due to volume discounts as they scale, see the following question and answer from their Q3 2023 earnings call:

Customers and Growth Prospects

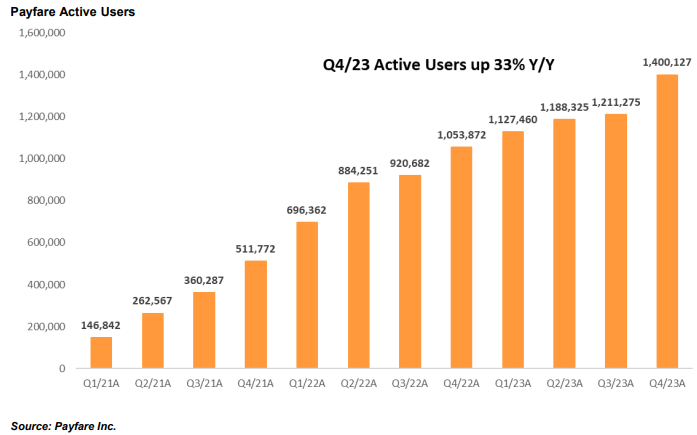

A couple charts on GDV and user growth from Payfare:

Although still experiencing strong revenue growth (~30% expected in 2024), growth has started to slow in recent quarters, primarily due to the law of large numbers — it becomes increasingly challenging to double revenues as the revenue base grows. However, I still see opportunities for Payfare to grow: (1) they currently have access to limited countries for each customer, providing opportunities for future expansion and growth to new countries; (2) they recently signed on two new customers at the beginning of 2024, with more hopefully in the pipeline; and (3) Payfare has optionality; they have 1.4 million (33% YoY) active users, as of Q4 2024, to whom they can sell new products and features.

Another aspect I like to see is small-cap companies with relatively large customers. This is one thing I liked about Civitanavi who signed an agreement with Honeywell (and was ultimately acquired by Honeywell).

Some of their large customers include:

Uber ($143.73B market cap); Payfare already works with them, but signed an additional contract in Q1 2024 to serve Canada.

ADP ($99.85B market cap); Payfare signed a contract with them to serve Canada in Q1 2024, with revenues and profits expected in 2025.

DoorDash ($53.37B market cap)

Lyft ($6.54B market cap)

ADP is an especially interesting customer to me because it diversifies Payfare beyond the gig worker economy and expands their total addressable market (TAM) to full-time workers. Imagine any worker getting access to money daily instead of every two weeks. ADP processes payroll for more than 1M clients worldwide, ranging from small businesses to global enterprise, however Payfare will only have access to Canada to start.

In general, I think it is a good strategy for Payfare to go through these large providers, such as ADP, instead of trying to market to individual businesses - imagine the customer acquisition costs if they went that route.

Now let’s talk about some of the risks.

Discussion on Risks (speculative)

I’ve included some of the bigger risks I can think of below:

The company has a few large customers, if any of them didn’t renew their contract it could dramatically impact revenues. Some mitigating factors:

Switching costs, it takes time to create a white-label solution and integrate the software with customers. Payfare starts with a smaller cohort of customers to test and then rolls it out to the rest of the user base. Once a customer becomes familiar with the app, there could be change management required to switch to a new offering.

The longer Payfare remains the chosen provider, the more their product improves through updates. Payfare gets the advantage of ironing out the quirks of what is essentially a new, currently non-commoditized, SaaS offering.

They don’t seem to be gouging customers - the fees and cash-back offerings look on par with good consumer credit cards and they don’t charge fees for some of their add-on services i.e. their back-up balance feature (up to $50 with no cost / interest).

Payfare white labels their offering (e.g. Uber or DoorDash branded card & app), perhaps this provides less incentive for a company to bring development in-house.

Accounting issues and reporting delays:

Looking through their historical financial statements I’ve seen a few restatements, however the ones I’ve seen don’t seem to affect the income statement materially. It isn’t ideal that their reports are delayed, but they have only been public for 3 years and accounting for a fintech company growing this fast could be tricky. I’m hoping there are less of these issues going forward.

Disruption / competition - any company that is as scalable as Payfare (from $1M in revenue to $186M in 7 years) is also disruptable; since they don’t need to reinvest a lot to grow, neither does the competition.

Payfare is currently heavily reliant on delivery drivers and if autonomous driving eventually works out maybe there would be less delivery drivers (maybe Payfare will be diversified by that time if this is far in the future?).

Regulation - I found this bill that could affect what fees Payfare can charge and there could be additional restrictive regulation passed relating to Earned Wage Access in the future.

Regarding insider selling, I reviewed the market buys and sells since the IPO in 2021. Due to never knowing for sure why anyone is selling, this section is highly speculative:

Kingsferry Capital Management Group Limited is the largest shareholder and appears to have been an early investor in Payfare. The group was heavily buying after the IPO, in 2021 and 2022, possibly expecting a significant increase in the share price as the company grew revenues by over 200% in both 2021 and 2022. Unfortunately in 2022 unprofitable tech names and microcaps took a large hit and not many companies were spared. In 2023, Kingsferry started heavily selling shares and now owns around the same amount as at IPO. There is always the possibility of increases in interest rates putting pressure on any borrowed shares. We will have to wait and see if they continue selling.

Co-founders, Marco Margiotta and Ryan Deslippe both also bought shares in 2021 after the IPO, and throughout 2023 have been participating in planned selling. Maybe they need the money or maybe they think the shares are going to fall – we can only guess.

Marco has slightly more shares than he did in the prospectus due to his sales being offset by market buys, options, and RSUs.

Founder, Ryan Deslippe, has about 20% less shares than in the prospectus.

Note: Kingsferry was a significant seller when the stock dropped 40% in Sept 2023.

Insider/founder ownership is 15% overall (24% including Kingsferry) which is good, and most insiders have not sold significant shares, including Keith McKenzie, the co-founder with the largest shareholding. The company also took advantage of low share prices to opportunistically buy back shares, which appears to have been a good move by management.

Summary

Payfare Inc is profitable with expanding margins, strong revenue growth, low capital intensity, and low customer acquisition costs — all at what I think is a fair price — there is a lot to like here. There is also some hair, like with a lot of small caps, and I can justify the risks all I want but there is real downside here. My current strategy involves a max initial allocation of 10% to any position (if it grows beyond 10% that’s fine) and Payfare currently sits at ~7% of my portfolio.

2024 Q1 earnings will be released next week, around May 8th. Although the new products with ADP Canada and Uber Canada were signed in Q1 2024, we shouldn’t expect to see significant revenues or profits until later in 2024 or 2025.

Disclosure: As of Apr 28, 2024, I am a shareholder of Payfare Inc at an average cost base of $6.24. My plan at the time of writing is to hold these shares long-term, but I may have sold my position by the time you’re reading this. This is not a purchase recommendation and I can only hope that I’m right on 3 out of 5 (60%) investments I make — this could be one I’m wrong on. Please do your own research and double-check my data & findings. Please also read my disclaimer and process here: Curious Investing Disclaimer and Process

What’s your sense of their ROIC (on a forward basis)—given the low maintenance capex it seems like the numbers should be absurdly high?

Sounds like it has a lot of upside but the top line may not grow as much for the next year at least. Lot's of volatility in tech and perhaps other investors are taking that into consideration given how relatively low the Price-to-sales ratio is. Risk it to eat the biscuit perhaps