Trustpilot Group PLC (LON:TRST)

Destination analysis, large TAM with strong competitive advantages

Current price (LON:TRST): $84.05 GBX

Current market cap (LON:TRST): $350.7M GBP

Link to my current public portfolio: Curious Investing Portfolio

Lollapalooza effects occur when there are multiple forces or factors moving in the same direction. The key is that when forces combine, they don’t just add up; each force builds off of and strengthens the other, creating an explosive effect with huge results.

—Charlie Munger

Trustpilot came public at the height of the recent tech boom, on March 26, 2021, at $265 GBX. After an initial rally to ~$450 GBX, the share price subsequently fell ~80% to its current price of $84.05 GBX.

What does Trustpilot do?

Trustpilot is an independent online review platform that allows consumers to leave reviews about both online and offline businesses. It provides a platform for customers to share their experiences and opinions on the products & services they have used.

Trustpilot aims to help consumers make informed decisions by providing a platform for genuine and unbiased reviews. Trustpilot's system is designed to promote transparency and credibility by allowing both positive and negative reviews. It also offers features such as user verification and moderation to help prevent fake or malicious reviews.

They have been quite successful in the UK and are expanding in Europe and North America.

Financial statements

Income statement:

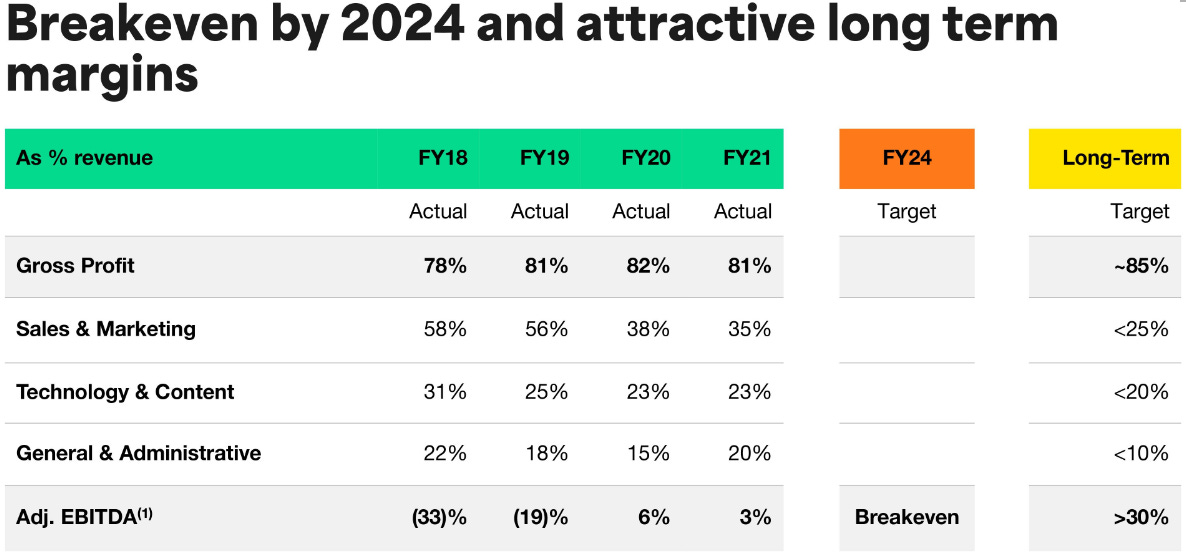

The company has 82% gross margins which is very high.

The company is inflecting on profitability and expects to be adj. EBITDA & FCF positive in FY2023.

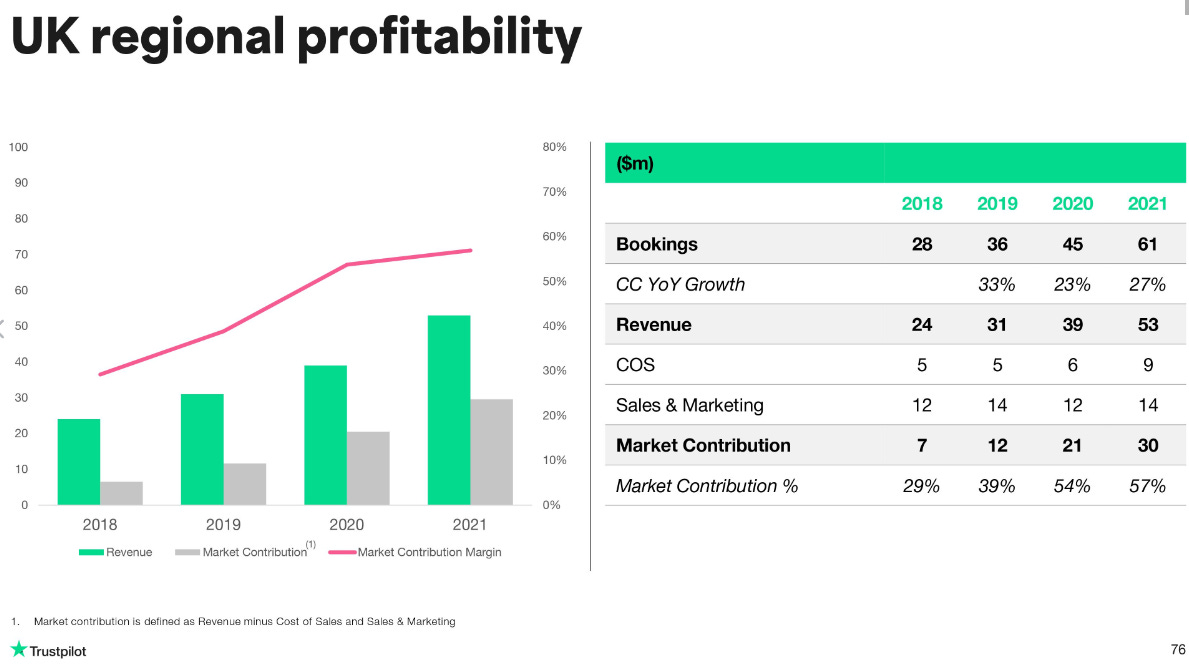

The company will exhibit operating leverage once profitable. Since a lot of their head office costs are fixed, aside from moderating reviews (fakes, bots, etc.), incremental revenue should increase faster than costs. The UK is Trustpilot’s most mature market and you can see below that profitability (market contribution) has increased as a % of revenue over time.

Balance sheet:

The company has $83M cash as of June 30, 2023 ($73.5M as of December 31, 2022) and expects to be adj. EBITDA and FCF positive in FY2023. It is plausible that the company will be able to self-fund from here.

Why I think Trustpilot could be a long-term compounder

Competitive advantage and flywheels:

Their business model has a strong competitive advantage which is required to compound earnings over long periods of time.

TrustPilot’s primary competitive advantage lies in network effects whereby businesses and consumers increasingly reinforce value for one another - as more consumers post reviews on more businesses, more businesses want to use the product and claim their domain, and then businesses invite even more consumer reviews. The more consumers and businesses using Trustpilot improves the product’s quality, attracting more consumers and businesses. (Flywheel #1)

It is rare to find network effects in small cap businesses.

Customers advertise for Trustpilot - businesses pay to include Trustpilot’s branding on their promotions online and at their physical store-fronts. So, as Trustpilot continues to grow and bring on more businesses, their brand recognition will grow as well (Flywheel #2). Not a lot of companies enjoy the benefits of this sort of subsidized marketing.

Tailwinds:

In the online age with consumers having an abundance of options, from entertainment to online storefronts, filters are increasingly important and they will continue to gain importance over time.

The total addressable market (TAM) for trustworthy reviews is large and anecdotally I think the number of consumers looking at third-party reviews before buying a good/service will increase over time.

Current competitors focus on smaller niches i.e. travel or local restaurants, but Trustpilot is relevant to all businesses. Their go-to-market strategy involves targeting high-potential industries in waves i.e. focusing on 3 to 5 industries at a time with marketing spend.

Independently verified reviews are good for society which is positive long-term.

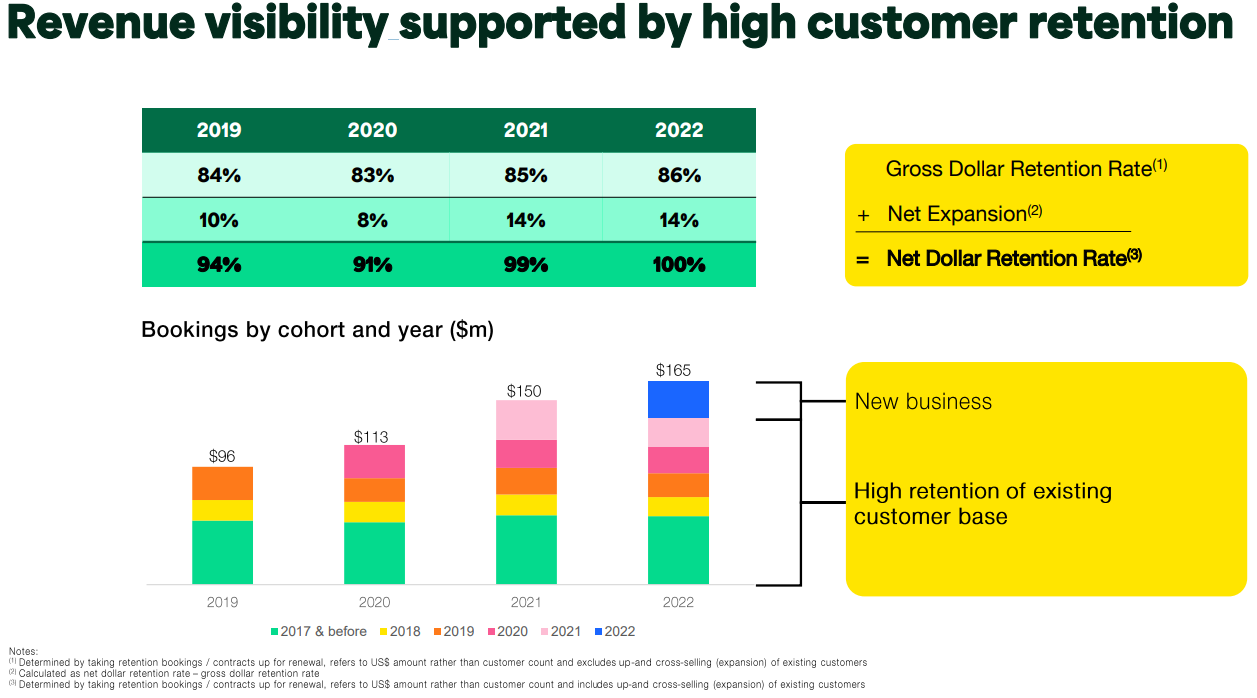

The slides below illustrate the value of Trustpilot’s product, which could lead to pricing power. Slide 1 breaks down their 100% net retention rates which drives marketing efficiency, increasing the Life-time Value of a Customer to Customer Acquisition Cost (LTV to CAC) …

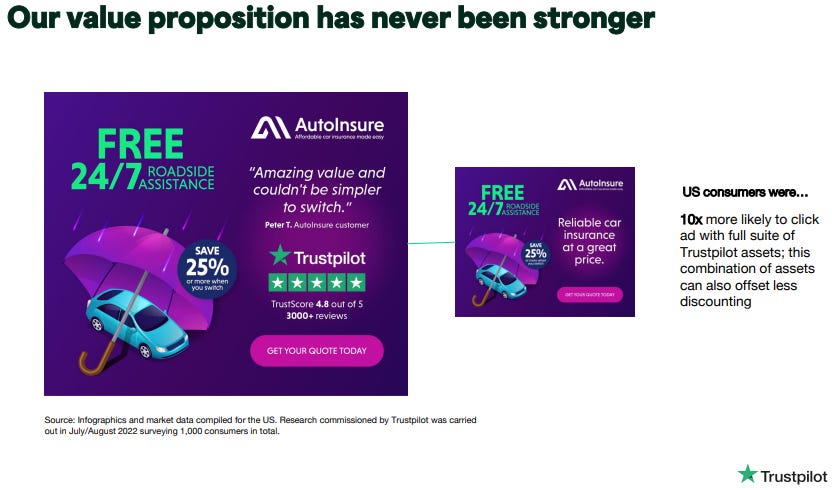

… and Slide 2 shows that simply including Trustpilot’s logo in an ad increases the likelihood a customer will click on an ad ~10x:

Risks & Opportunities

(1) Competition: There are already a few larger companies competing to provide third-party reviews in targeted niches / industries:

Yelp (reviews for local restaurants and services) is currently at a $3.12B USD market cap.

TripAdvisor (travel reviews) is at a $2.32B USD market cap.

Sites like Yelp and Tripadvisor make most of their money from advertising and promotion of businesses on their site, which could be viewed as a conflict of interest. It wouldn’t be surprising if a company paid these sites to take down bad reviews or promote good ones.

While Trustpilot may not grow their revenues as fast by avoiding this conflict of interest, I would argue this is a long-term advantage for them - being independent will increase the quality of their product (reviews) in the eyes of the consumer who value transparent and trust-worthy experiences.

(2) Low insider ownership: The CEO, Peter Mühlmann, is the most significant insider with ~2% ownership (counter-point: this is likely a substantial portion of his net worth). Trustpilot started as an unprofitable VC company where it is typical for insiders to be diluted prior to IPO. Low insider ownership can lead to agency issues.

(3) New CEO as the company transitions from hyper-growth to self-funding and operating leverage: Peter is stepping down and there is a new CEO Adrian Blair starting in September 2023. Adrian was Global Chief Operating Officer ("COO") of Just Eat from 2011 - 2018 and served throughout Just Eat's journey from a startup (£30m revenue) to the FTSE 100 (market cap £5.5bn, 2018 revenue of £780m)

From 2019 to 2022, Adrian was Chief Executive Officer of Dext, a leading SaaS accounting automation platform. Under Adrian's leadership the business trebled the number of users around the world, and delivered significant product innovation, gross margin and bottom line improvement. Most recently, he was Chief Business Officer of Cera.

Here is an interesting article he wrote on LinkedIn: https://www.linkedin.com/pulse/how-jitse-groen-won-adrian-blair/?trackingId=MtG0q1vbSHW1ynIiE425xA%3D%3D

(4) Float characteristics: Trustpilot collects payment at the beginning of contracts, on average 6 months in advance, and provides their service later which leads to positive working capital contribution.

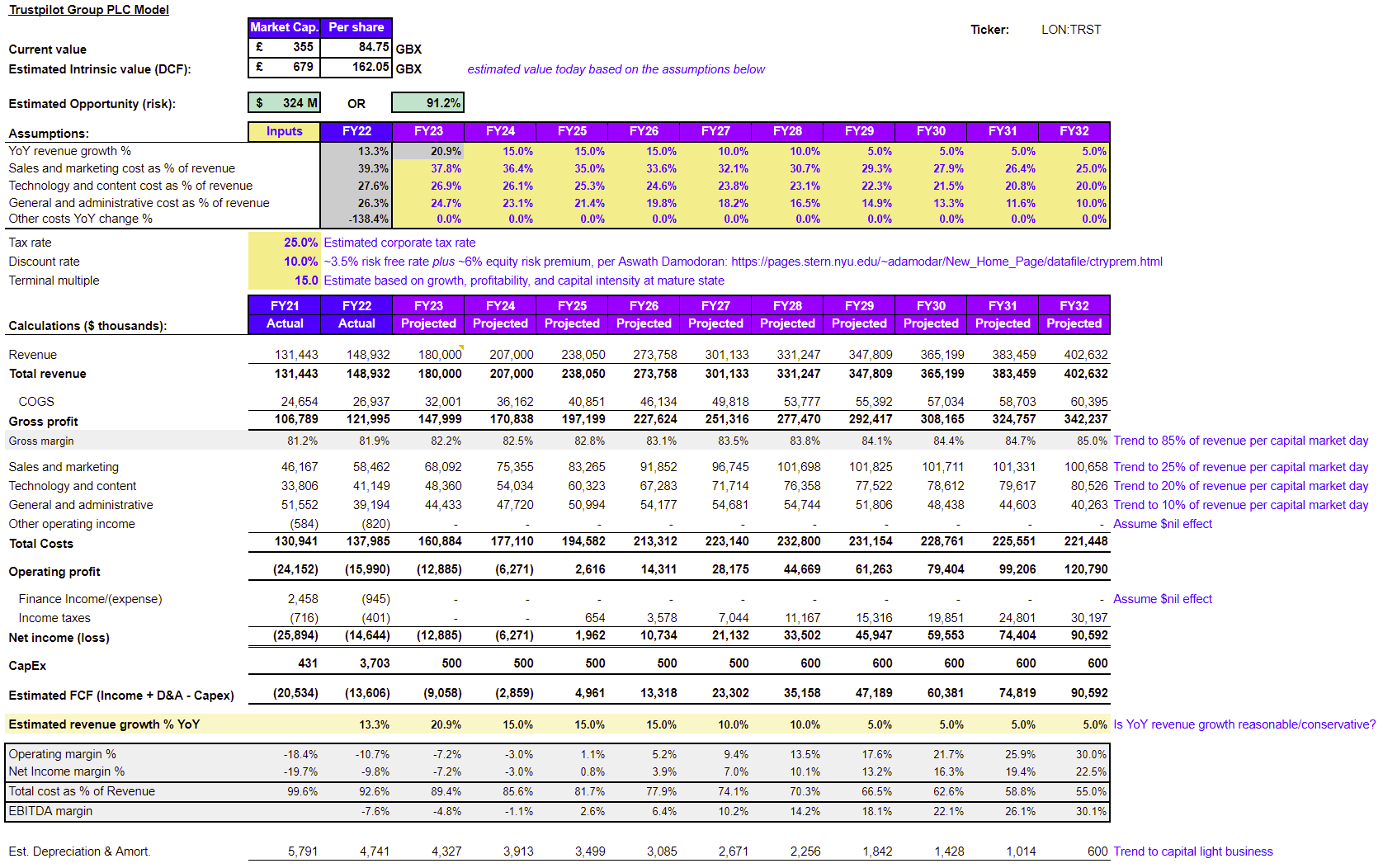

Valuation

It is difficult to value companies in the self-funding / operating leverage stage of the business life-cycle, so I try to picture what the company will look like 10 years out (destination analysis). In my opinion Trustpilot will be much bigger than they are today because they have high-quality and long-term focused attributes including their flywheels, competitive advantage, and general industry tailwinds.

(1) Multiple-based valuation:

Valuation multiples are a function of a five factors; the three business-related factors include:

Growth rate:

Trustpilot is growing revenue in the high teens YoY in a tough advertising environment (OK).

Profitability profile at steady state:

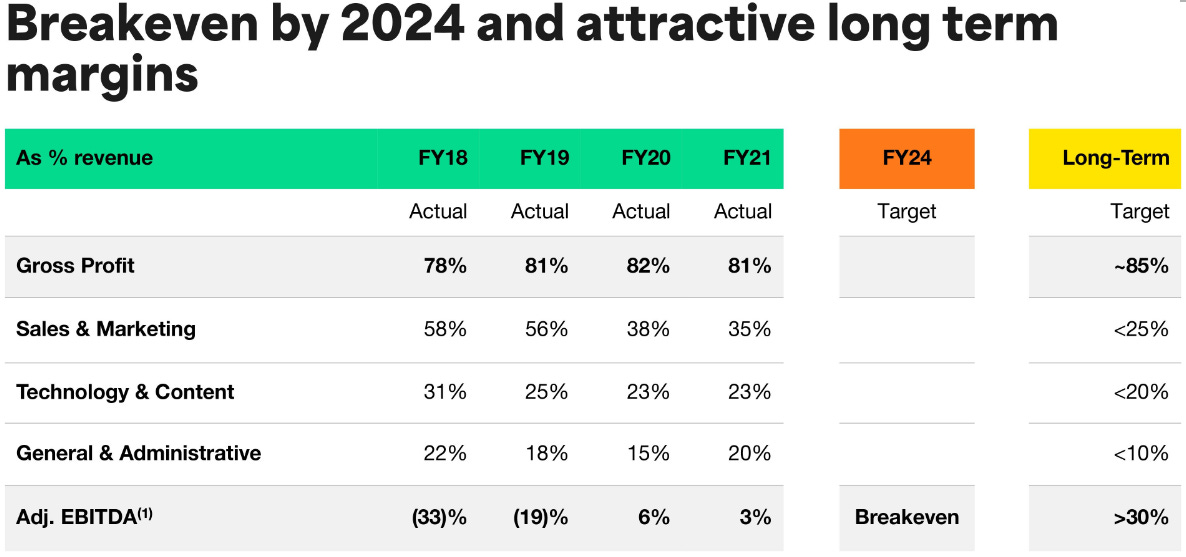

82% gross margins are very high and indicate the company could have high operating margins once mature (Good). Per their capital market day slide below, they are targeting 30% adj. EBITDA long-term and I’ve included these targets in the DCF below.

Capital intensity (maintenance capex):

Trustpilot’s business is capital light (Good).

Other factors, primarily out of the control of the business:

Market conditions (macro and equity risk premium).

Risk of complete failure (black swan).

Trustpilot currently trades around 2.0 EV to sales which I think is quite low for a business with the attributes and prospects detailed above.

(2) DCF-scenario-based valuation:

I’ve also put together a quick model for fun using the long-term assumptions they included in their capital market day presentation above, assuming they gradually approach those targets as a % of revenue in year 10. These numbers illustrate a scenario in which the company could be undervalued today, but won't come close to actual results and doesn’t give them credit for their positive working capital. I've included the assumptions so you can assess yourself whether they are too aggressive or conservative.

Below are the results with a discount rate of 15%:

Disclaimer: As of August 7, 2023, I am a shareholder of Trustpilot Group PLC at an average cost base of $85.95 GBX. My plan at the time of writing is to hold these shares long-term, but I may have sold my position by the time you’re reading this. This is not a purchase recommendation and I can only hope that I’m right on 3 out of 5 (60%) investments I make — this could be one I’m wrong on. Please do your own research and double-check my data & findings.

Late to this party. One question for you on the incentive alignment: isn’t it arguably more problematic that businesses pay Trustpilot for services on the platform? That seems like a stronger conflict than just advertising on the platform.

The valuation does appear to be a big opportunity. Thx again Mr. Curious Investor!