Zedcor Security (ZDC or Zedcor Inc)

Great unit economics and strong demand -- using technology to disrupt traditional security

We believe the greatest investments of our time are companies that we call "Rule Breakers," because they break the rules of the business status quo. Rule Breakers bring a disruptive technology, diabolically clever marketing, or a totally new business model into the world, and they rattle our capitalistic foundations. In so doing, they can create serious profits for the opportunistic investors who find them early on.

— Motley Fool (David Gardner)

I have been posting about Zedcor on MicroCapClub, a private investment group, and I want to summarize my thoughts here as well.

Note: I have also started sharing some of my other MicroCapClub forum posts in the Curious Investing blog’s chat if I don’t feel it warrants an article of it’s own.

Zedcor price today (Jul 28, 2024): $1.52 CAD

My cost basis: $0.52 CAD

Market cap: $130.24M CAD

Zedcor is one of the larger investments in my portfolio at 7%. The stock has almost tripled since my original posts in December, but I still believe in the long-term investment case.

Here is a link to my public portfolio in Google Sheets where I record my buy & sell activity: Curious Investing Portfolio

What does Zedcor do?

Zedcor Inc., formerly known as Zedcor Energy Inc, is a Canadian company that provides security and surveillance solutions. They specialize in offering mobile surveillance units and security services to various industries. Their solutions are designed to protect assets, deter crime, and ensure safety on job sites.

This is a simple business — they set up towers with motion sensors and remotely monitor them at a central location. They can speak through the towers to deter would-be thieves and call the police. You may have seen some of theirs, or competitors’, security towers in parking lots. They look like this:

Business Highlights

They are experiencing rapid growth — with 70 towers in operation at the end of 2021, approximately 950 towers in operation as of March 31, 2024 and 1,300 to 1,500 expected by the end of 2024. So far the towers have greater than 90% utilization rates.

Zedcor is active with offices across Canada and recently entered into the US, initially in Texas with plans to expand to more states. Colorado has now been announced as well.

They earn revenue through monitoring services. Zedcor owns the tower, sets it up on customer sites, and then charges a recurring monitoring fee (high margin).

They have announced projects with Home Depot (started with 10 locations and recently expanded to 23 stores / distribution centres + 13 projects under construction) and the “largest homebuilder in North America” (I’m assuming this is DR Horton per Google search).

They have started manufacturing their own towers in Houston, lowering their cost per tower.

Zedcor is working on wall or pole mounted cameras, currently in beta, and they already have an order for 100 units. These should be less capital intensive and hopefully also come with a monitoring (high-margin) contract attached.

Competitive Advantages of Towers vs Traditional On-site Security

This is a new way of doing security that I think has structural advantages over typical security (having a guard on site) – it is cheaper, scalable, and able to more efficiently / safely monitor sites. It is difficult to tell when a new way of doing things will truly disrupt and it can take a long time in capital intensive businesses, but if the cost of the remote monitoring for a customer is less than the cost of shrinkage and on-site security, then the market should continue to grow.

On-site security guards also come with liability to the employer — this is one reason security guards are asked not to intervene when someone is stealing something (so the employer isn't sued if they get hurt).

The capital intensive nature of the business gives competition more time to enter the market, but also keeps out new competition once the business is mature and has scale (Zedcor isn't close to scale yet).

Some signs of security towers being a disruptive technology:

Per management, they opened operations in eastern Canada 2 years ago and it already makes up 33% of their revenue;

Zedcor has mostly maintained revenue while Transmountain (previously their largest customer) has wound down from 190 towers to 30 towers (160 towers is 17% of their 950 fleet); and,

Their high utilization rates (greater than 90%) indicate they are putting every tower they get their hands on into the field.

Security Tower Unit Economics

Zedcor is a simple business at its core, buy or produce a security tower and rent it to someone with a monitoring service contract. But we still need to determine if each incremental tower bought/produced provides a sufficient return on investment.

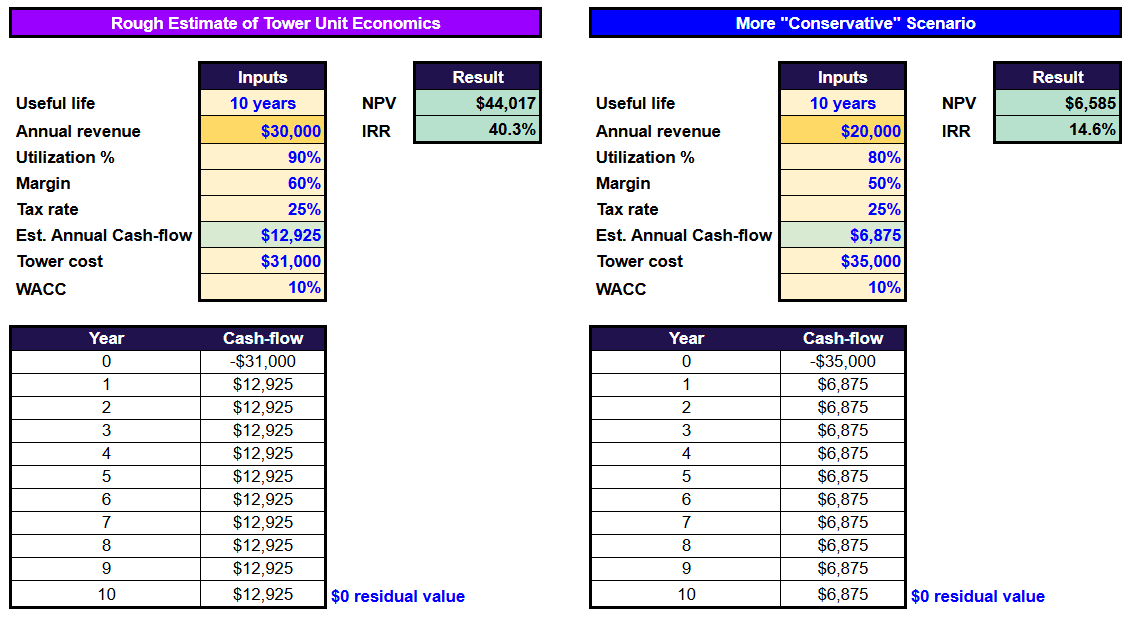

Here are my rough assumptions:

During my initial research, in an older YouTube interview, their CFO didn’t directly state their margins, but implies the recurring revenues are highly profitable (>50%). And per their FY23 and FY24Q1 financials, they had > 60% gross margin (excluding tower depreciation).

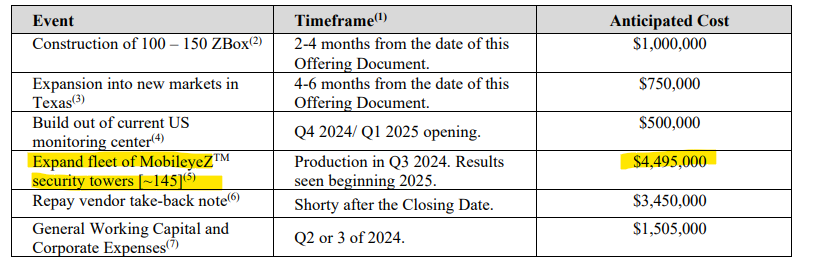

In their most recent financing we can calculate their estimated cost per tower at $31K ($4,495,000 / 145)

In their latest presentation they quoted $30K revenue per tower per year ($2,500 per month), but larger companies may be able to negotiate lower rates. Let’s assume 90% utilization.

Tower useful life of 10 years and disposal value of $0 (guesses on my part, somewhat informed by depreciation rates).

Here are two simple calculations:

Based on these calculations Zedcor’s tower unit economics appear quite strong (40% IRR) → this implies that Zedcor will earn a 40% return less their cost of capital (cost of debt or equity) on every dollar invested.

Even in a much more conservative scenario with $20K annual revenue per tower, 80% utilization and 50% margin, the company would still be making money (15% IRR) although the returns wouldn’t be as jaw-dropping.

Competition will put downward pressure on Zedcor’s margins, but we should also see some scale benefits as they grow e.g. if they can reduce manufacturing costs or extend the useful life of a tower.

Here are management estimates of unit economics from the following Smallcap Discoveries presentation:

I'm having trouble reconciling their numbers because a 24 month payback period implies higher than 24% ROIC to me; someone let me know if I'm missing something.

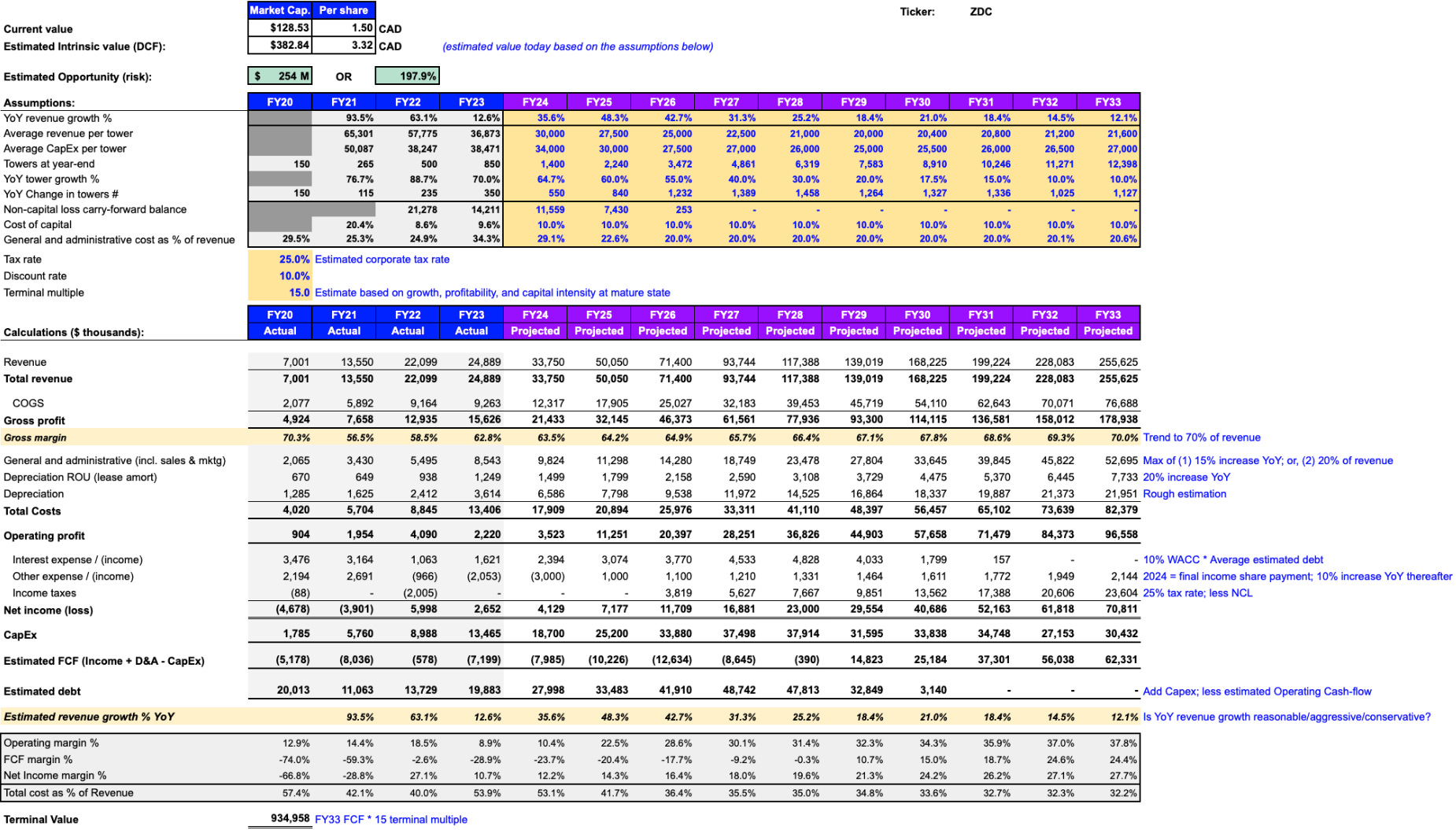

Valuation Based on Q1 and Today’s Price

The company has run up since my original purchase, but the calculations below have been updated for today’s prices.

I’ve put together a model for fun using very high level assumptions. These numbers illustrate a scenario in which the company could be undervalued today — a sanity check — but won't come close to actual results. I've included my assumptions so you can assess yourself whether they are too aggressive or conservative.

Note: Most of the estimated intrinsic value is driven by the terminal value in year 10. It is difficult to accurately forecast 1 or 2 years in the future, let alone 10, that is why we can only use models like this as a sanity check.

Risks

(1) Competition with Other Security Tower Providers (Moat): Even if we think security towers are better than on-site security there isn’t much stopping other companies from entering the sector other than capital constraints, as there is nothing proprietary about these towers. So their direct competition with other security tower providers is likely the biggest risk to this investment. However, I like that:

Zedcor is public, which allows more flexibility for funding;

The biggest competitors are primarily focused on remote monitoring & towers — they may have their focus split between different types of security offerings, including on-site security guards. These competitors would have to cannibalize their sales in one offering to make the switch — a tough proposition for a public company (innovators’ dilemma).

Zedcor is starting to vertically integrate by manufacturing their own towers. "On January 9, 2024, the Corporation announced that Zedcor Manufacturing (USA) completed design work on its 2024 Solar MobileyeZ model ... The Corporation is now in full production of the 2024 model and is able to currently produce 30 to 40 MobileyeZ a month at its Houston facility with the intention to ramp up production to 100 security towers a month by Q3 2024"

It is impressive how quickly they got manufacturing operations up and running, already producing 30 - 40 per month, but this also means a competitor could quickly ramp up production as well.

I don’t think that Zedcor needs to be a first mover to capture enough growth to be a good investment and, anecdotally, I think the remote monitoring sector will have tailwinds (growth) for years to come.

(2) Insiders: The largest insider Dean Swanberg (Board Member with 21.6% ownership) is selling shares — there are many reasons an insider can sell shares, sometimes neutral and sometimes bad, but never good.

The second largest insider is the CEO Todd Ziniuk with approx. 2% ownership.

One thing to look out for companies with low management ownership is agency issues i.e. when management enriches themselves over shareholders — I don’t see anything concerning in this area for Zedcor.

(3) Financing/Equity Offerings: Zedcor recently issued $15M worth of shares at $1.00 share. If Zedcor wants to grow to meet demand they will need financing through debt or equity. The market generally doesn’t like financing, but based on Zedcor’s unit economics it could be a good long-term decision for the company. However, if the terms of the financing are unfavourable i.e. with warrants attached or equity raises at unfavourable prices, this could turn into a long-term risk.

Zedcor’s current financings appear to be under reasonable terms, so hopefully they can obtain similar going forward.

(4) Dilution: Related to the above two points, there has been significant dilution over the last few years as Zedcor has transitioned from energy services to security. They have raised funds for growth and granted significant option and RSU packages.

We should hope that dilution slows down going forward (excluding equity raises specific to building additional towers when the stock price is “expensive”, and ideally with no warrants & minimal transaction fees).

As little dilution as possible, or even a reduction in share count, is always good for shareholders.

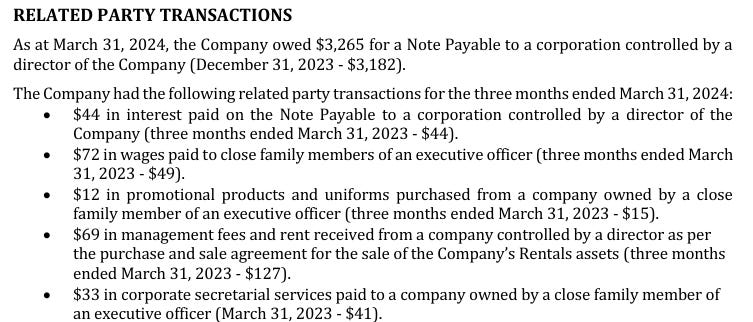

(5) Related party transactions: I don’t think there is anything here to be alarmed about, but something to keep an eye on (the $3.3M note has since been paid back):

(6) Demand dries up: Zedcor has plans to build manufacturing capacity for up to 100 towers a month by FY24Q3, which equates to 1,200 per year. As of FY24Q1 they had a fleet of 950.

Can they generate enough demand for that many towers?

If the project with Home Depot continues to go well, Home Depot has 182 locations across Canada, 184 locations in Texas (where ZDC is operating in 2024), and ~2,300 stores in the US (side note: the scale of US vs Canada is incredible — one state has more locations than all of Canada).

They mentioned in a press release they are working with the largest homebuilder in North America (D.R. Horton?) so if you believe home building is going to have strong tailwinds over the next decade, which I do, that is a good thing.

Just these two companies could keep Zedcor busy, but Zedcor’s sales team will keep working on signing new customers along the way.

Summary

You won't find many microcaps in large-market industries with ironclad competitive advantages (because by the time it is obvious the company will be much larger), but you also don't need one to get a more than acceptable return.

If my thesis is right (it may not be) — that these remotely monitored security towers disrupt on-site security due to being cheaper, a better deterrent, and/or less liability — then growth & adoption could follow an s-curve with the total addressable market for on-site security shrinking while the market for remotely monitored towers increases. Zedcor only needs to capture a small portion of this growth to be a good investment.

Disclaimer: As of July 28, 2024, I am a shareholder of Zedcor Inc. at an average cost base of $0.52. I am not an investment or financial advisor. My plan at the time of writing is to hold these shares long-term, but I may have sold my position by the time you’re reading this. This is not a purchase recommendation and I can only hope that I’m right on 3 out of 5 (60%) investments I make — this could be one I’m wrong on. Please do your own research and double-check my data, findings, and calculations. Please also read my disclaimer and process here: Curious Investing Disclaimer and Process

As someone without a finance background I appreciate your posts being consistently written with a level of lead in and/or explanation that allows me to understand even the most complex terms and topics you discuss.

Regarding Zedcor would you ever consider an increase in property crime or building construction investment a useful indicator?

Interesting thesis. I will look at the valuation numbers. If your assumptions are reasonable (and they look like they’re) there’s a long runway ahead.

Penetration to the US was a challenge and the agreement with HD was their way in. They are quite heavily dependent and their customer base is too concentrated, hopefully there’s a plan to address this risk